The pursuit of streaming profitability over subscriber numbers has seen the major studio groups turn their attention to content licensing deals. The sweet spot is finding the balance between exclusivity and non-exclusivity, and in the case of non-exclusivity using that content to drive licensing revenue.

New research published by Ampere Analysis shows that after four years of major studios employing a walled-garden approach to the distribution of their TV content on streaming, licensing is steadily making a comeback.

Between 2019 and 2021, media company studios s began to pull content from Amazon and Netflix and other licensing partners prior to debuting their own SVODs, ensuring that content exclusivity was a major part of their launch proposition. A notable move was WarnerBros’ removal of Friends from Netflix ahead of HBO Max launch.

“Having content exclusively available particularly when its hugely popular or part of major franchises can help when building a brand at launch and therefore helps in penetrating an increasingly competitive market,” said Rahul Patel, research manager at Ampere Analysis.

Now the industry is moving to a new period where cross licensing is becoming a lot more common. “This also reflects the state of maturity these platforms are reaching,” Patel told StreamTV Insider. “They now better understand what content is keeping consumers engaged or attracting new subscribers and what other content can be additionally monetized through cross licensing.”

Ampere’s analysis highlighted significant recent increases in catalog overlaps between different platforms. Netflix and Warner Bros. Discovery, for example, started 2023 with 22 TV seasons shared between them and ended the year on 68 (including HBO/Max shows Band of Brothers, Insecure, Ballers).

Amazon Prime Video and Peacock’s season overlap jumped from 156 to 275 in the same period (including Mon, Chicago Fire and Chicago P.D).

Its data also illustrates the scale of popular content that has been retained by the studios “highlighting the potential and room for growth in licensing.”

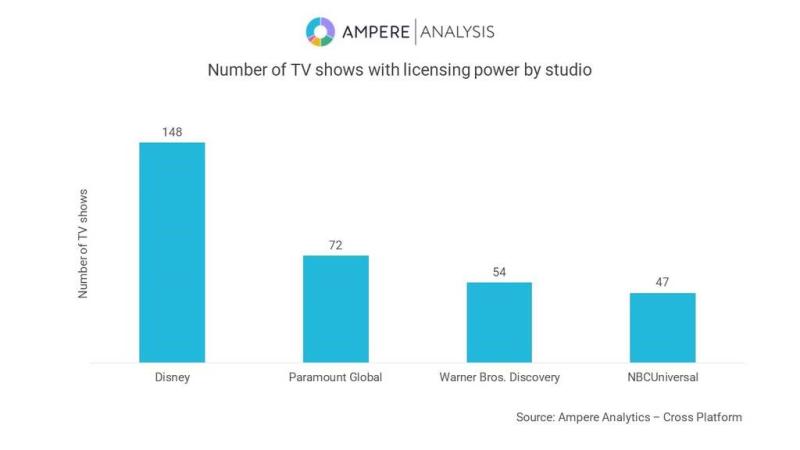

Disney has most muscle here with 148 TV shows identified as having licensing power still only available on its platforms at end of 2023. That is about to change when a major Netflix deal for around 14 Disney and Fox series rolls out on Netflix between now and January 2025, including Prison Break, and How I Met Your Mother. This totals in excess of 90 TV seasons.

For context, Ampere data shows Netflix and Disney+/Hulu had an overlap of 152 TV seasons in Decemeber2023, up just 13% from January 2023’s 134. So the deal in its entirety represents a big change.

Paramount has the second largest cache of high value content. Star Trek and its spin-offs are core to the Paramount brand and are understandably retained exclusively for Paramount+ but these “also reflect some of the most popular licensing assets if they choose to go down that route,” said Patel.

AVOD platforms are also licensing partners. NBCUniversal has been most active in this area, sharing the most content not just between SVOD platforms but also with AVOD platforms. WBD is distributing over 2000 hours of its content, including through Warner Bros-branded FAST channels on Tubi and The Roku Channel.

Ampere’s research also shows that studios are considering changing their strategy around core IP exclusivity. WBD for instance has been very protective of its theatrical slate, in contrast to Paramount and Universal whose theatrical releases have often landed on other platforms a few months after the first pay window, noted Patel. “Yet in Q3 last year WBD licensed a whole host of its movies to Amazon including DC titles and then rolled them out to Netflix and Tubi for limited periods.”

Reaching wider audiences through licensing

While the principal driver to cross license is for increased revenue, another benefit for studios is to reach wider audiences with their content.

“I see licensing as part of a marketing tool,” Patel said. “It’s not by accident that Warner Bros. licensed a set of DC titles to other platforms like Amazon and Netflix on the eve of releasing Aquaman 2 at the end of last year.”

WBD is also featuring its Oscar winning hit Dune prominently on Netflix in the run up to the sequel’s release next month.

“By licensing these franchise titles to platforms with a large audience, studios can market to more people and hope for a positive return as more people engage with content in its original home.”

AMC+, a far smaller streamer, sought the wider reach of Max when it created a ‘streaming pop-up’ on Max to carry seven AMC series for two months beginning September, including Anne Rice’s Interview with the Vampire and Killing Eve.

WBD itself will be hoping to engage new audiences in seeing Sex and the City revival series, And Just Like That, on Max after making all six seasons of HBO’s original series available from April on Netflix.

Similar activity has not yet been witnessed by Apple TV+ which seems to be pursuing a policy of quality of quantity when it comes to content.

Ampere’s analyst doesn’t rule out a change in Apple’s strategy, particularly given the shifting chairs of bundles, mergers and acquisitions in the industry.

Amazon, meanwhile, has licensed some unscripted originals to WBD for distribution on broadcast TV in some EU markets in what Patel called “another change in the playbook for streaming originals.

“Netflix meanwhile is at the forefront of the streaming game and perhaps calculates less of a need to license out content,” he said. “It has found other avenues to generate revenue such cracking down on password sharing and the launch of its ad tier.”

The industry can expect more licensing deals for high profile titles to be struck in 2024 between major VOD providers. Patel added that cross licensing can be seen “as a first step in wider partnerships between platforms” as the industry reshapes itself with bundles, mergers and acquisitions.

Broadcaster, SVOD overlap ahead for the European market

Ampere’s research is based on the U.S SVOD market and the conditions around exclusivity around what the studio and streamers catalog looked like at the end of 2023.

“The walled garden approach is slightly differently in Europe because some of the major U.S streamers aren’t operating in certain markets,” said Patel. Peacock, Hulu, Max for example have not launched in the UK. Ampere will publish research in the market later this year.

However, Ampere predicts more licensing between UK broadcasters and streamers following that between Disney and UK commercial broadcaster Channel 4 which saw ten Disney series including Abbott Elementary and X Files made available to the broadcaster’s eponymous streaming platform.

ITV continues to strike carriage deals with Warner Bros for TV and on streaming platform ITVX including the Harry Potter franchise and The Vampire Diaries.

Patel said, “We expect the partnership and overlap between broadcaster led VOD and SVOD platforms both in the UK and other major European markets to increase, in the same way we are seeing cross licensing between major SVOD providers in the U.S.”